This calculator computes the value of Equated Monthly Installments (EMI) for user specified values. Just enter the values for Rate of Interest, the Amount of Loan required, Tenure (in years) and specify whether you would like to use an Annual , Monthly or Daily Reducing balance for the calculations and click on the Calculate button. The Result will be displayed in the box named EMI.

Inherent Investment Potential With a population approaching the billion marks by the turn of the century, real estate in the Indian sub-continent has obvious potential for growth. While the idyllic Indian village life has an emotional appeal, the discerning investor knows the importance of easy accessibility to schools, hospitals, shops, offices, entertainment centers and airports. A real estate investment has far higher value in the major towns and cities of India. A wise investment here can benefit from the historic movement of population to urban centers. A process of economic liberalization has also encouraged NRI investments into real estate with the advantage of repatriation of the capital invested and even the rental proceeds under the circumstances prescribed by RBI.

Reserve Bank has granted general permission to certain financial institutions providing housing finance e.g. HDFC, LIC Housing Finance Ltd., etc., and authorized dealers to grant housing loans to non-resident Indian nationals for acquisition of a house/flat for self-occupation subject to certain conditions. The purpose of the loan, margin money and the quantum of loan will be at par with those applicable to housing loans to residents. Repayment of loan should be made within a period not exceeding 15 years out of inward remittance or out of funds held in the investor’s NRE / FCNR / NRO accounts.

Reserve Bank permits Indian firms/companies to grant housing loans to their employees deputed abroad and holding Indian passports subject to certain conditions.

Reserve Bank has granted general permission to foreign citizen of Indian Origin to acquire or dispose of properties up to two houses by way of gift from or to a relative who may be an Indian Citizen or a person of Indian origin whether resident in India or not, subject to compliance with applicable tax laws.

Reserve Bank has granted general permission for letting out any immovable property in India. The rental income or proceeds of any investment of such income are eligible for repatriation.

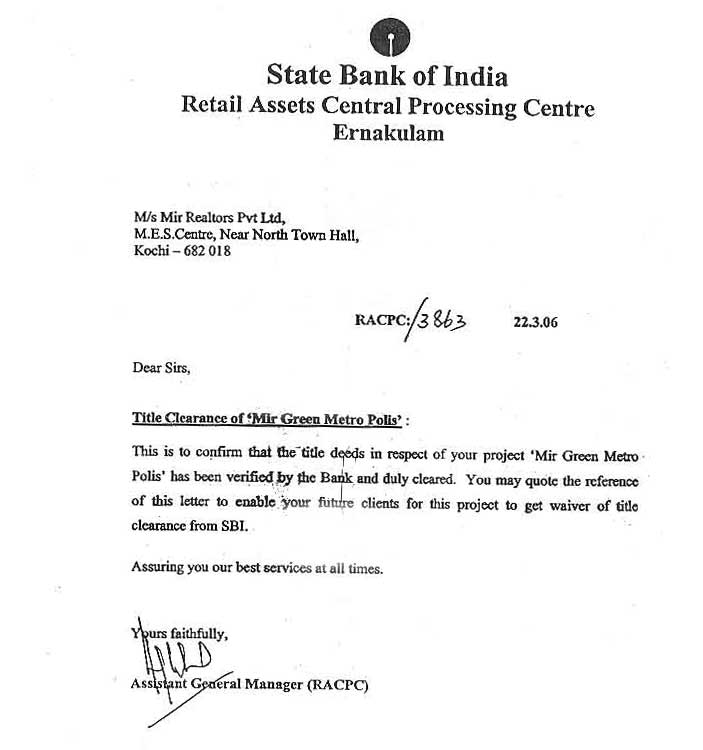

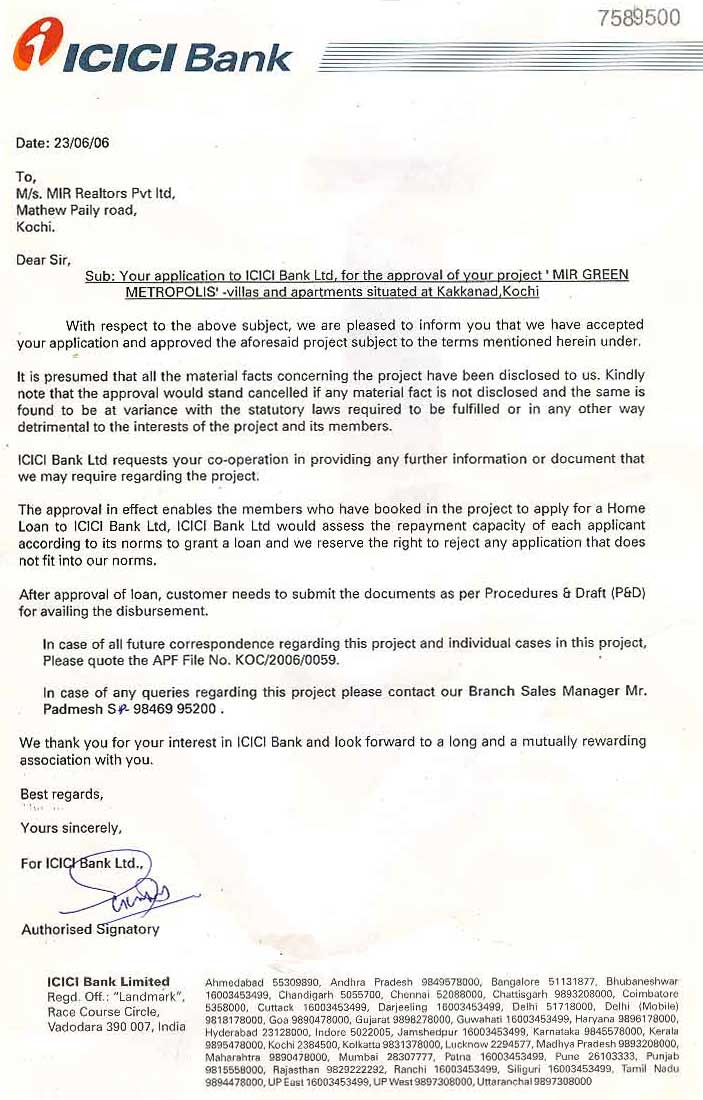

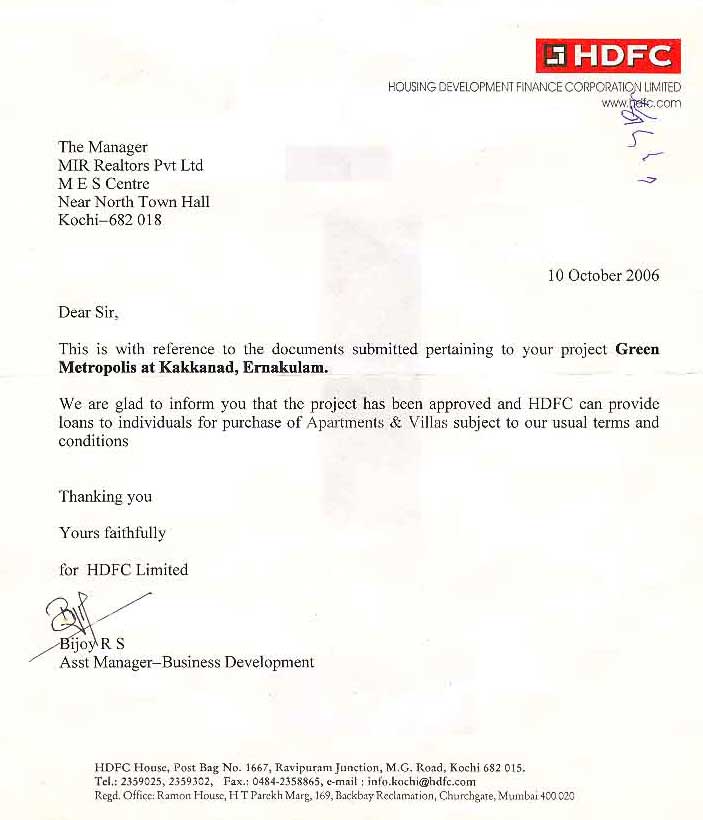

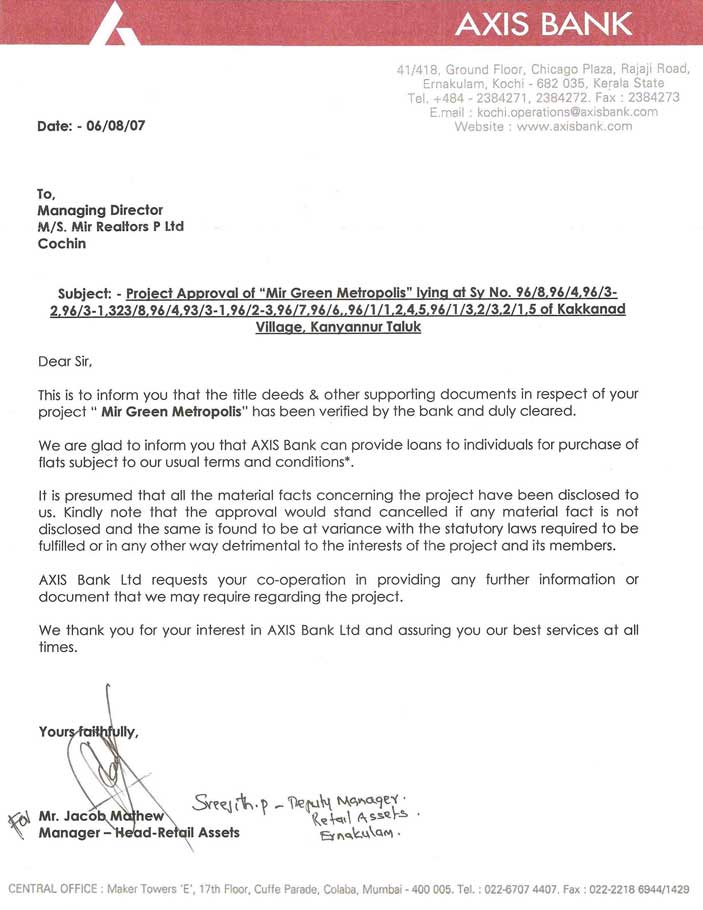

We shall help you finance your desired living space at Mir Realtors through suitable home loans from HDFC, ICICI and AXIS Bank. We are here to help with your home loan needs every step of the way – right from educating you about the types of home loans available and the formalities involved to securing a suitable loan for you. However, having an understanding about the nuances and formalities involved in acquiring a home loan could come in handy.

For Resident Indians: Various factors like income, age, educational qualification, current liabilities, total assets, spouse’s income and more are taken into consideration to determine the eligibility of a home loan applicant. The general eligibility norms applicable for the Resident Indians include:

For NRIs: Though the eligibility criterion set for the NRIs is similar to that of resident Indians, more emphasis is given on the following when it comes to the appraisal of an NRI case.

For Resident Indians:

For NRIS:

The following fee and charges are attached with home loans processing.

Copyright © 2025 Mir Realtors. Powered by Phenomtec